![]()

![]()

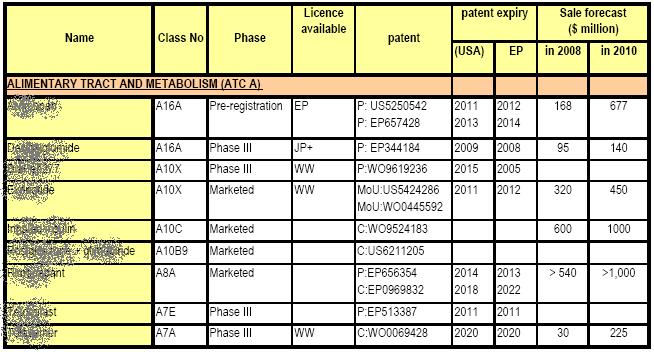

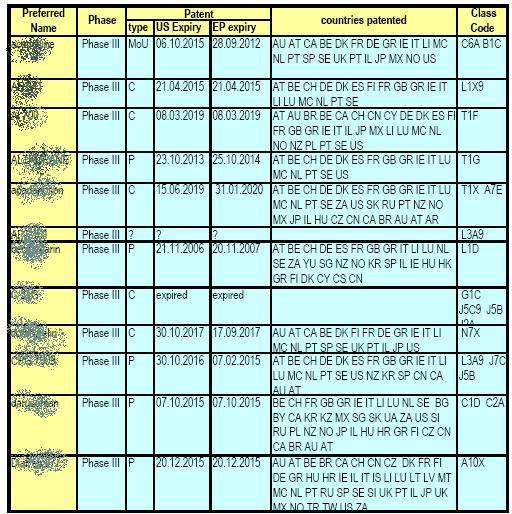

Please contact us for the whole list in all therapeutic groups, at any level of

development (Phase I, II, III, pre-registered etc) and with can submit you a full

world-wide or only for a particular country patent report, license details, etc.

Technical Assistance:

PLEASE LET US KNOWN WHICH THERAPEUTIC CLASS ARE YOU interested in ? What are the molecules are you planning to compete with? WE WILL TRY TO FIND THE WAYS OF CIRCUMVENTING PATENT(s), if any of them is a barrier for a generic launch. We will let you know as soon as possible, if it can be possible with an alternative formulation or by employing different salt or polymorph or hydrate or other means by considering the very important fact of yielding bioequivalent alternative to the innovator's.. Of course, the resulting product would be less cost involving that would make you well compatible in the market upon launch that could be foreseen by our break even point analysis. We can also search Process market situations for earliest launch possibilities, such as for the AT BR, CN, CR, CZ EE, FI, GR, HU, IN, LV, LT, NO, PO, RO,RU, SK and SP, where molecules can not patent protected until a certain year so that generic launch can be realized with a proper process as long as indication ( MoU) is not limiting.

| A quick browse to Japanese Market: |

-

The 2nd largest market & largest in Asian market as US$ 67.7 billion in 05 from 64.4 in 04.

-

Share of generics is extremely low as low as 16-17% when compared with those in the USA, 51%, the UK 52% and Germany 50%.

-

Generics 17% of sales by volume but market share just 6%.

-

5% growth 04 to 05

-

Economic expansion 2.6% in 04 & 2.6% in 04

-

Population ageing: >65 old 3.3 million, dependency ratio 34.6% an alarming level

-

Btw 07 to 10 of 8% workforce retire, age moved to 65.

-

FTA signed with ML TH & MX.

-

Healthcare reforms- cost-limiting activities increased.

-

40 % of market by ten companies.

-

Among the innovators, Takeda leading with a sales growth of 8.5%& market share 6.4%.

-

Dainippon+Sumitomo, daiichi+sankyo merged in 05.

-

Sales force Pfizer is the biggest 3200 MR, Asteillas 2500, Takeda +150 on 05 to 1700, Dainippon+Siumitomo 1500 MR’s.

-

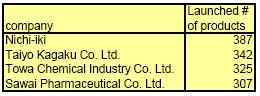

As far as generics are concerned, Towa, Taiyo, Sawai and Nichi-iko > 432 new generics added to NHI price list in 05.

-

All 4 launched Takedas lansoprazole & voglibos, Astellas tamsulasin.

-

Agreegate sales of 3 >1.3 billion US $..

-

Taiyo s annual revenues> US$ 250 million.

-

190 versions of 29 active ingredient exposed to generic , were launched in 05. More than 80 generic companies..

-

Sawai (43.6%), Towa (30.1%), Nichi-Iko (29.5%), Merck Hoei (28.3%), and Taiyo (22.5%).

-

-

substitution of generics for brands, reference pricing, etc have not yet been implemented.

-

complete separation of prescribing and dispensing medicines has not occurred, 48% of medical institutions both prescribe and dispense pharmaceutical products, contrast to both the USA and the EU, where complete separation exists

-

Medical institutions that gain profits from the gap between the purchasing and reimbursement price still tend to use brands with higher profit margins than generics; however, the push to promote the use of generics has just started.

-

Several obstacles to quick access to, and market penetration.

-

HOWEVER, Revision in Pharmaceutical Affairs Law (PAL) in april 2007, is a great opportunity now!.